Suntrust recently hobbled the card, which was a real heartbreak for those of us who'd gotten one when it was still available. But, interestingly, Suntrust has now revived the card for new applicants and is even offering a sign-up bonus (a modest 5,000 Skymiles).

The value proposition is much lower with the new restrictions, but it could be interesting to some folks.

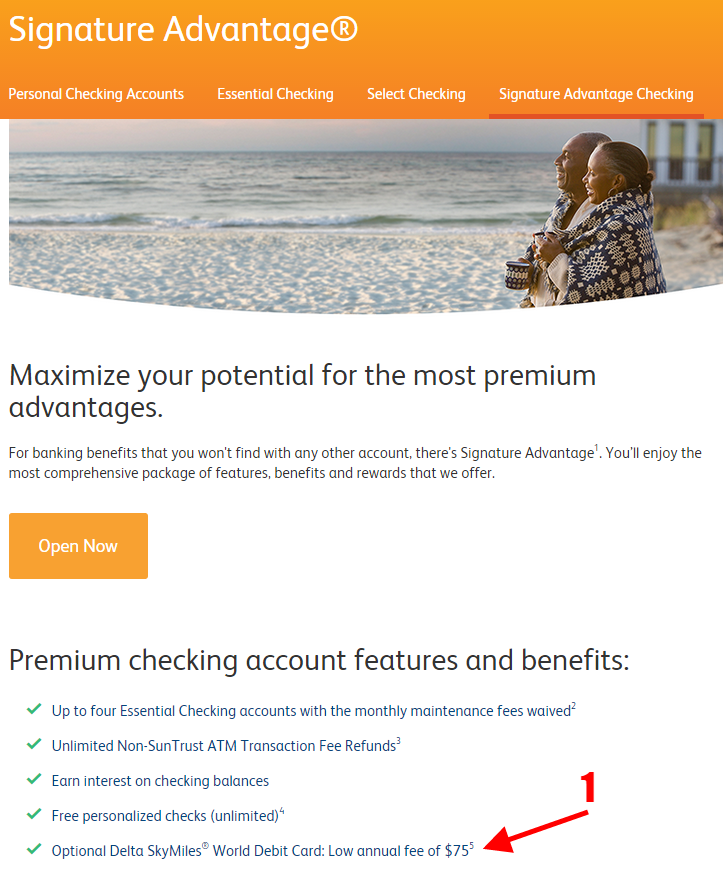

It appears that for new accounts, the card is available only to Signature Advantage or Premier Banking accounts:

In addition to the $75 annual fee for the card, Signature Advantage accounts carry a $25 monthly maintenance fee. That fee is waived if you maintain a minimum deposit balance of $25,000 including IRAs, and investment accounts:

Under the new terms, a Delta Debit Card attached to a Signature Advantage checking account earns 1 Skymile per dollar spent, including PIN-based transactions. However, you are limited to earning 4,000 Skymiles per month.

Just as a mental exercise, let's suppose you had an IRA or investment account that you could transfer to Suntrust to avoid the monthly maintenance fees. This scenario assumes no opportunity cost for moving that money to Suntrust, i.e. that you'd get the same rate of return with them. If you maxed this deal out, your return would look like this:

- Cost: Annual fee of $75 + cost of MSing $48,000 in PIN-based transactions (approx. $35-50) = $110-$125

- Return: 53,000 Skymiles (Signup bonus + 1MPD)

- Cost per Skymile: $0.002 or .2CPM

That's not too bad, since I generally value Skymiles a a little over 1CPM. Given the hard upper limit on earning, I probably wouldn't jump at this deal myself. Still, it's worth considering, particularly if you live in Suntrust's service area. Of course, it you happen to already have $25,000 on deposit with Suntrust, I'd say jumping on this card would be a no-brainer.

UPDATE: Some folks on the Flyertalk thread dedicated to this card have speculated as to whether one can have more than one Skymiles Debit Card per account. The answer is yes:

BUT, there doesn't appear to be any reason to do so, as the Ts&Cs state that: "Enrollment and all bonus miles are only applicable once perclient/checking account and SkyMiles number." The terms also indicate (but don't unequivocally state) that the monthly earn limits are per account, not per card.

BUT, there doesn't appear to be any reason to do so, as the Ts&Cs state that: "Enrollment and all bonus miles are only applicable once perclient/checking account and SkyMiles number." The terms also indicate (but don't unequivocally state) that the monthly earn limits are per account, not per card.

UPDATE to the UPDATE: Oooh. This just got more interesting. Via chat, a Suntrust agent confirms that the limits are "per card" limits, NOT "per account" limits. That means a single joint checking account could carry up to three cards (which must be linked to three separate Skymiles accounts) and earn 4,000 miles per month PER CARD. I'll be interested to see if this pans out. If it does, joint account holders could each earn 48,000 miles per year on without each having to deposit $25,000. The agent also confirmed that that secondary Skymiles Debit Cards would not incur an additional annual fee (but would not be eligible for an additional cap) if both cards were linked to the same Skymiles account.

UPDATE: Some folks on the Flyertalk thread dedicated to this card have speculated as to whether one can have more than one Skymiles Debit Card per account. The answer is yes:

UPDATE to the UPDATE: Oooh. This just got more interesting. Via chat, a Suntrust agent confirms that the limits are "per card" limits, NOT "per account" limits. That means a single joint checking account could carry up to three cards (which must be linked to three separate Skymiles accounts) and earn 4,000 miles per month PER CARD. I'll be interested to see if this pans out. If it does, joint account holders could each earn 48,000 miles per year on without each having to deposit $25,000. The agent also confirmed that that secondary Skymiles Debit Cards would not incur an additional annual fee (but would not be eligible for an additional cap) if both cards were linked to the same Skymiles account.